Determining the main tax domicile of legal entities that operate in different areas of tax jurisdiction or have no or only marginal operational business activities is particularly challenging. The article in "EXPERT FOCUS – October 2025 issue: 'Principal tax domicile of legal entities' shows how carefully this location is assessed and how practice is increasingly focusing on the criterion of "actual management" in particular (Di Giulio / Kaufmann / Braun, 2025). If there is no discernible geographical focus of management or key corporate decisions for localizing the actual management, it cannot automatically be assumed that the actual management of the company is located at the place of residence of the managing director. The localization of the main tax domicile often leads to discussions in practice and is particularly important in the context of avoiding intercantonal and international double taxation.

Legal basis

The following relevant provisions apply to legal entities:

Federal Act on the Harmonization of Direct Taxes of the Cantons and Municipalities (StHG), Art. 20 para. 1: Unlimited tax liability in a canton where the registered office or actual management is located.

Cantonal regulations: For example, in the canton of Bern: Tax Act of the Canton of Bern (StG BE), Art. 76 StG BE: "Legal entities are liable for tax on the basis of personal affiliation if their registered office or actual administration is located in the canton."

Principle of personal affiliation: The statutory registered office may be decisive, but if the actual administration is concentrated in another location, that is where the main tax domicile is located.

Principal tax residence – what matters?

The main tax domicile refers to the canton/municipality that is primarily responsible for assessing a legal entity. The decisive factor is where the actual administration takes place: where the key decisions are made, where the management is based, and where operational management is carried out.

Criteria for actual administration:

Who makes the key corporate decisions (e.g., management, board of directors)?

Where are day-to-day business activities conducted (accounting, controlling, operational management)?

Is there only a statutory registered office without any actual activity (mailbox)?

Were clear structures created, with management decentralized across several cantons or countries?

Latest developments

Federal Supreme Court 9C_547/2023 of April 8, 2025

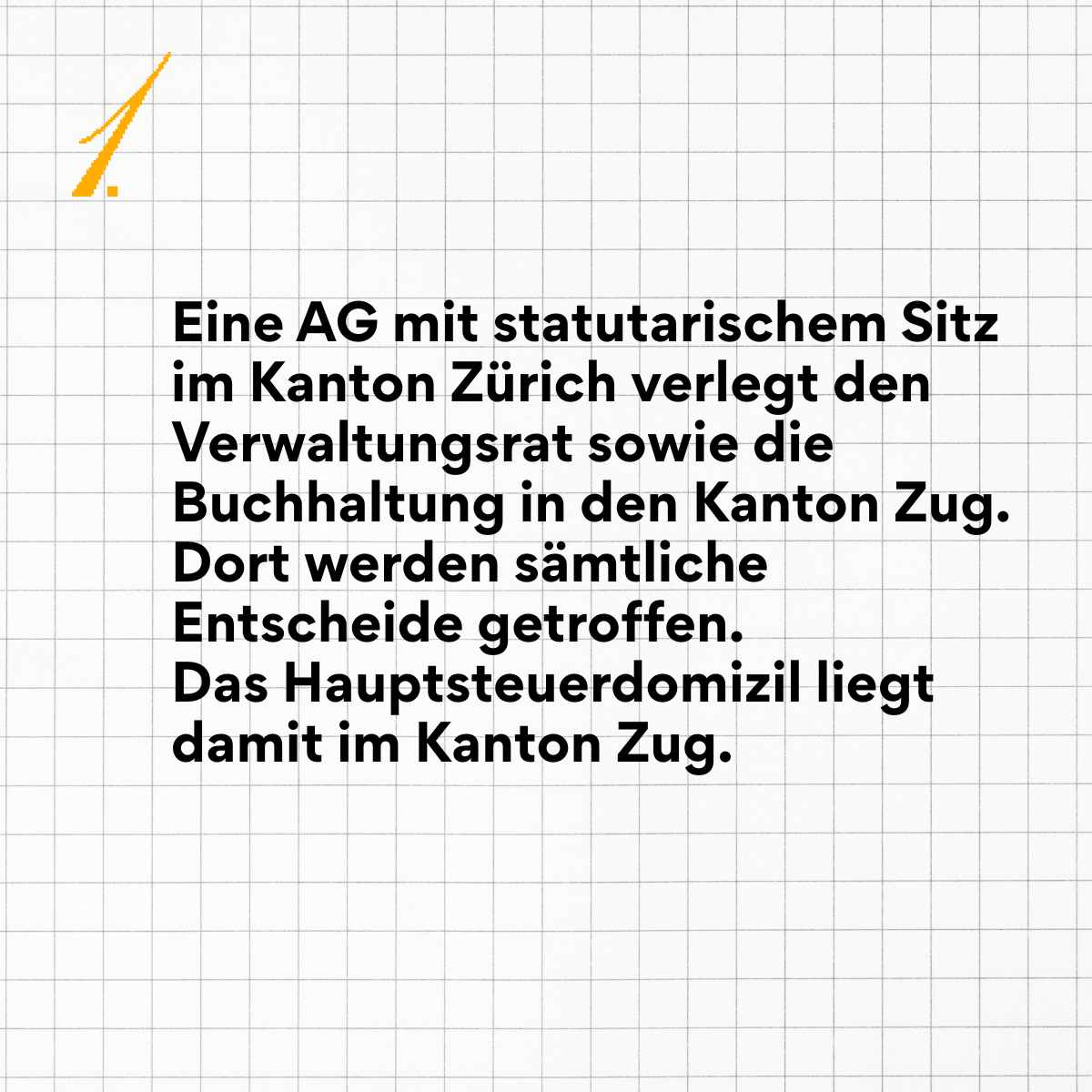

In decision 9C_547/2023, the Federal Supreme Court ruled that the legal entity (referred to in the proceedings as "A._ AG") was not liable for tax in the canton of Zurich, even though the sole member of the board of directors was resident there. Instead, the main tax domicile was located in the canton of Zug.

Key points of the ruling:

The lower court had assumed that the management was based at the domicile of the board of directors in Zurich. However, the Federal Supreme Court found that no clear geographical focus of management had been proven.

In the absence of such evidence, the place of residence of the managing director may not automatically be considered the place of effective management. This meant that Zurich's tax jurisdiction was revoked.

Significance: The ruling shows that tax authorities cannot automatically assume the place of residence of the board of directors if the operational management is located elsewhere or cannot be clearly proven.

Examples:

Double taxation between cantons

Two cantons may wish to tax the same company for the same tax period. This is possible due to Switzerland's federal structure. However, it contradicts the principle of the intercantonal prohibition of double taxation (Art. 129 para. 3 of the Federal Constitution).

In practice:

If two cantons claim that the main tax domicile is located in their territory, this results in double taxation.

In this case, the company could potentially receive two assessments for the same period, which is a risk.

Tax authorities and courts therefore carefully examine which canton actually has tax jurisdiction based on the above criteria.

In its decision 9C_489/2024 (dated May 1, 2025), the Federal Supreme Court clarified that the prohibition of intercantonal double taxation does not automatically lead to a revision of a legally binding assessment.

recommended actions

Check at an early stage whether your company is actually managed at its registered office.

Document clearly: location of management, board of directors, accounting, decisions.

If management is spread across multiple tax jurisdictions: Determine the geographical center of gravity and record this in business documents.

If you are unsure about your main tax domicile, contact your tax advisor, especially if you are involved in intercantonal or cross-border activities.

Are you relocating your registered office or management? Make sure that the entire tax period is taken into account (unity of the tax period) – changes can have retroactive tax consequences.

Conclusion

The location of a legal entity's main tax domicile is more than just a formal registered office entry: it is about the economic reality and the place of actual management. The Federal Supreme Court's ruling 9C_547/2023 clearly shows that the place of residence of the managing director is not automatically the place of actual management if there are no clear indications to that effect. For your company, this means ensuring consistency between the articles of association and the actual management – because misinterpretations can lead to uncertainty, double taxation, or subsequent reassessments.

what customers say about us

"With humor and joy!"

I founded my company with adminster. I am very satisfied! Will now continue to work with them.

M

Michael Dettwiler

adminster then gave us a helping hand with their expertise and ensured that we no longer just had the right turnover, but that our accounting was also in line with legal requirements.

If you are looking for a partner in the area of finance and accounting who can ensure that everything in this area is as it should be in an uncomplicated and independent manner, then adminster is an ideal partner.

H

Hans Geeler

Very professional and reliable service. The adminster team works quickly and precisely and offers expert advice. We have been working with them since the beginning and have been able to see how a start-up has become a really great SME. I am very satisfied with the collaboration and can recommend the service without reservation!

M

Marco Licini

We have been working with adminster since this year and are surprised by the good quality. By quality we mean digital processes, direct communication and excellent advice at a fair price. Absolutely top!

P

Physio Schenk

Professional support in all areas with extremely friendly people. I can recommend adminster fiduciary who wants straightforward, competent, and reliable support.

M

Madleina Speich

I have been working with adminster for years and am completely satisfied. Whether accounting, payroll administration, taxes or business consulting - I always receive competent, fast and reliable support. The collaboration is personal, professional and solution-oriented. For me, they are the first port of call for all financial and administrative matters. Highly recommended!

S

Sat To

We have been working with adminster for over 1.5 years now. They do most of the bookkeeping for us. The cooperation with Simon and his team is very competent, reliable and on an equal footing. We are very satisfied!

J

Jesse Gerner

I've been working with Simon and his team for almost 3 years now. It has been a pleasant experience all the way. As a lean start-up, we try to do the maximum by our own (As it is the cheapest). Simon supported us in this effort and never gave me the feeling of being a complete newbie (despite making many and repetitive mistakes). I recommended Simon already to multiple other start-ups and companies and had great feedback from them as well.